|

|

| | |

|

Life Insurance Basics

|

|

Note:

Variable life insurance policies are offered by prospectus, which you

can obtain from your financial professional or the insurance company. The prospectus

contains detailed information about investment objectives, risks, charges, and expenses, as well as the underlying investment options.

You should read the prospectus and consider this information carefully before purchasing

a variable life insurance policy. | |

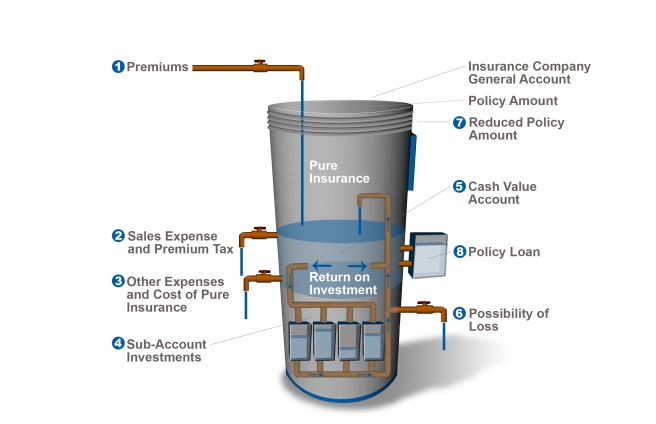

How Variable Universal Life Insurance Works

- You decide (up to limits regulated by federal tax law) when and how much premium

payment to "pour in." The minimum premium is based on insurance company sales expenses,

premium taxes, and the cost of pure insurance for your policy.

- As you pay your premium, the insurance company deducts its sales expenses and premium

taxes.

- The remainder of your premium is credited to your cash value account. Each month,

the company charges this account for its other expenses and the cost of pure insurance

(net amount of risk coverage), or mortality cost.

- You choose the subaccounts in which your cash value is invested. These accounts

are securities-based, though many policies offer a fixed account option.

- Growth in your subaccount investments can "pump up" your cash value.

- With the potential for growth comes the possibility of loss. If your investment

choices perform poorly, your cash value could go "down the drain."

- If your remaining cash value is not sufficient to cover expenses and the cost of

pure insurance, and you do not pour in more premium, the policy amount may then

have to be reduced, or your policy will lapse. This would be similar to crushing

the container at the top.

- You may take a policy loan in an amount not to exceed the policy's cash surrender

value less the annual loan interest. Repayment replenishes your cash value, but there may be a tax liability if the policy terminates before the death of the insured. Any

loan balance outstanding (plus interest due) at your death is deducted from the

policy amount paid to your beneficiary.

|

|

|

|

|

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual's personal circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

This communication is strictly intended for individuals residing in the state(s) of AL, AK, AZ, AR, CA, CO, CT, DE, DC, FL, GA, GU, HI, ID, IL, IN, IA, KS, KY, ME, MD, MA, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NY, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, UT, VT, VI, VA, WA, WV, WI and WY. No offers may be made or accepted from any resident outside the specific states referenced. |

| Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2024. |

|